517 Credit Score Problem: A Dream Business Stuck on Hold

Securing a business loan often hinges on a single, crucial factor: your credit score. But what if your score isn't where it needs to be? This is exactly what Alex is going through, one of our credit repair clients.

Alex had a vision. He wanted to launch his own business—a step that could completely change his financial future. But there was just one problem standing in his way:

💰 He needed a $100,000 loan to fund his startup.

📉 His credit score was 517.

The bank told him he needed a 680+ credit score to qualify. A 163-point gap felt impossible.

Alex had no idea where to start. Should he pay off collections? Open a new credit card? Wait and hope his score improves over time?

For a long time he was thinking of ways to increase his credit score for his dream business loan. The clock was ticking, and every day he wasn’t approved meant he was losing money and opportunities.

Why a 517 Credit Score is a Red Flag for Business Loans

A 517 credit score isn't just "low," it's a significant barrier to securing business financing. Here's why:

🚩High Risk Indicator: Lenders view a 517 score as a strong indicator of financial instability and a high probability of default. In the world of business loans, where larger sums are at stake, lenders are extremely risk-averse.

🚩Limited Loan Options: With a 517, traditional banks and credit unions are likely to deny your application outright. Your options become severely limited, often pushing you towards high-interest, predatory lenders. You might want to check our article about Easiest Credit Union to Join with Bad Credit.

🚩Unfavorable Terms: Even if you find a lender willing to work with you, expect “skyrocket” interest rates and harsh repayment terms. This can strangle your business's cash flow and hinder its growth potential.

🚩Business Credit Impact: Personal credit scores often influence business creditworthiness, especially for startups and small businesses. A low personal score can cast doubt on your ability to manage business finances responsibly.

🚩Lack of Trust: Lenders rely on credit scores to assess your financial reliability. A 517 score erodes that trust, making it difficult to build a strong lender relationship.

🚩Delayed Growth: As in Alex’s case, low credit scores delay business growth. The time spent trying to find financing is time that could be used for building the business.

Every point below that 680 threshold was a missed opportunity. Every day he waited, his competitors gained ground. As for Alex, he wasn't just facing a loan denial; he was facing the potential loss of his entire business dream.

Alex learned that a 517 didn't just mean "no loan." It meant limited options, higher interest rates if he found a desperate lender, and a constant uphill battle. It meant his personal credit was casting a long shadow over his business aspirations.

The Common Credit Score Trap

Like most people, Alex assumed the only way to improve his score was to:

❌ Pay off old collections

❌ Dispute everything negative

❌ Open new accounts and “build history”

🚨 But here’s the truth: These aren’t the fastest or most effective ways to boost a credit score.

Alex had already tried disputing negative items, but nothing changed. He had paid off some collections, but his score barely moved. He was stuck—until he found a better strategy.

Good Read: How Robert Got a $2,160 Verizon Bill Removed—And His Dream Home Approved

The ASAP Credit Repair Strategy: A Smarter Approach to Credit Growth

Instead of using basic disputes or wasting money paying off bad debt, we built a custom strategy designed to get him to 680+ fast. We were able to grow his 517 credit score in no time.

Here’s what we did:

📌 Step 1: Targeted Account Deletions

We analyzed his credit report line by line and found:

- 4 errors in how negative accounts were being reported

- 2 collections that were past the legal reporting timeframe

- 1 charge-off that lacked proper documentation

Instead of just “disputing” these, we challenged the original creditors for full documentation. They couldn’t provide it.

🔥 Within 60 days, 3 accounts were removed.

📌 Step 2: Strategic Credit Rebuilding

💡 Did you know your credit score isn’t just about removing negatives?

We helped Alex build new, positive credit by:

✅ Adding authorized user accounts (giving him instant credit history)

✅ Opening a high-limit secured card (with the right type of utilization)

✅ Guiding him on reporting rent payments to credit bureaus

🔥 Within 90 days, his credit score jumped 120 points.

📌 Step 3: The Final Push to 680+

At this point, Alex was close—but not quite there.

His final hurdle? A stubborn late payment from 2 years ago.

We used the CEO Method (Challenge → Escalate → Overturn) to legally remove the late payment.

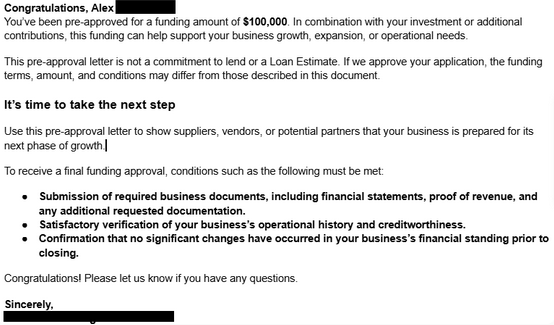

🔥 Final Score: 692.

🚀 Loan Approved.

Here’s Alex’s Pre-Approval Letter:

The Aftermath: Business Funding Secured

✅ Final credit score: 692

✅ $100,000 business loan secured

✅ Dream business launched

Instead of waiting years for his score to improve, Alex hit his goal in under 4 months.

What made the difference? He didn’t waste time on methods that don’t work. He followed a proven strategy designed to get real results.

Same 517 Credit Score and Struggling to Get Approved?

A 517 credit score is honestly not a good number when...

✅you dream of expanding your business,

✅buying a home,

✅or simply accessing better financial opportunities.

A score this low severely limits your options, locking you out of favorable interest rates and crucial approvals. It's time to face the reality of a subprime score and understand how to climb out of the hole.

Whether you need a loan, a mortgage, or just better credit opportunities, there’s a smarter way to improve your score.

🔹 Start a chat with us now → [Click Here]

🔹 Call us at 📞 888-656-0803

🔹 Text us at 📲 281-545-5001