Quick Summary

Fh Cann and Associates is a legitimate debt collection company that's been operating since 1999. If they're on your credit report, you owe (or allegedly owe) money to one of their clients. Your options: dispute the debt if it's wrong, negotiate a settlement (often 30-60% of original amount), or pay in full. You can stop their calls with a cease and desist letter. Always request debt validation within 30 days and know your rights under the Fair Debt Collection Practices Act.

Finding Fh Cann and Associates on your credit report can be stressful. I’ve written extensively on debt collection, and I know how damaging these accounts can be. A single collection can drop your score by 50 to 100 points, sometimes more.

So, I took time to share my knowledge about Fh Cann and Associates and how we at ASAP Credit Repair deal with collectors like them.

The good news? You’ve got options like validation, dispute, even removal if the debt can’t be verified.

But here’s the bad news: if you don’t respond the right way, this account could continue to drag your score down and sit on your report for up to 7 years.

Who Is Fh Cann and Associates?

FH Cann & Associates (also called FHC) is a debt collection company. They started in 1999 and have been collecting debts for over 24 years. They're based in North Andover, Massachusetts.

The company is a certified Woman-Owned Business. They don't just collect debts. They also run call centers and help other businesses with their operations.

Company Contact Information

- Address: 1600 Osgood St Suite 2-120, North Andover, MA 01845

- Phone: (877) 750-9801

- Website: www.fhcann.com

- Years in Business: 24 years (since 1999)

Better Business Bureau Rating and Reviews

FH Cann & Associates is BBB accredited, but their rating changes based on complaints. Common complaints from consumers include:

- Communication Issues: Too many calls, wrong numbers

- Debt Validation Problems: Not providing proper proof

- Payment Issues: Problems with payment processing

- Credit Reporting Errors: Wrong information on credit reports

What Other Consumers Say

Most reviews mention:

- Positive: Professional staff when you reach the right person

- Negative: Difficulty reaching someone, persistent calling

- Mixed: Some successful settlements, others had problems

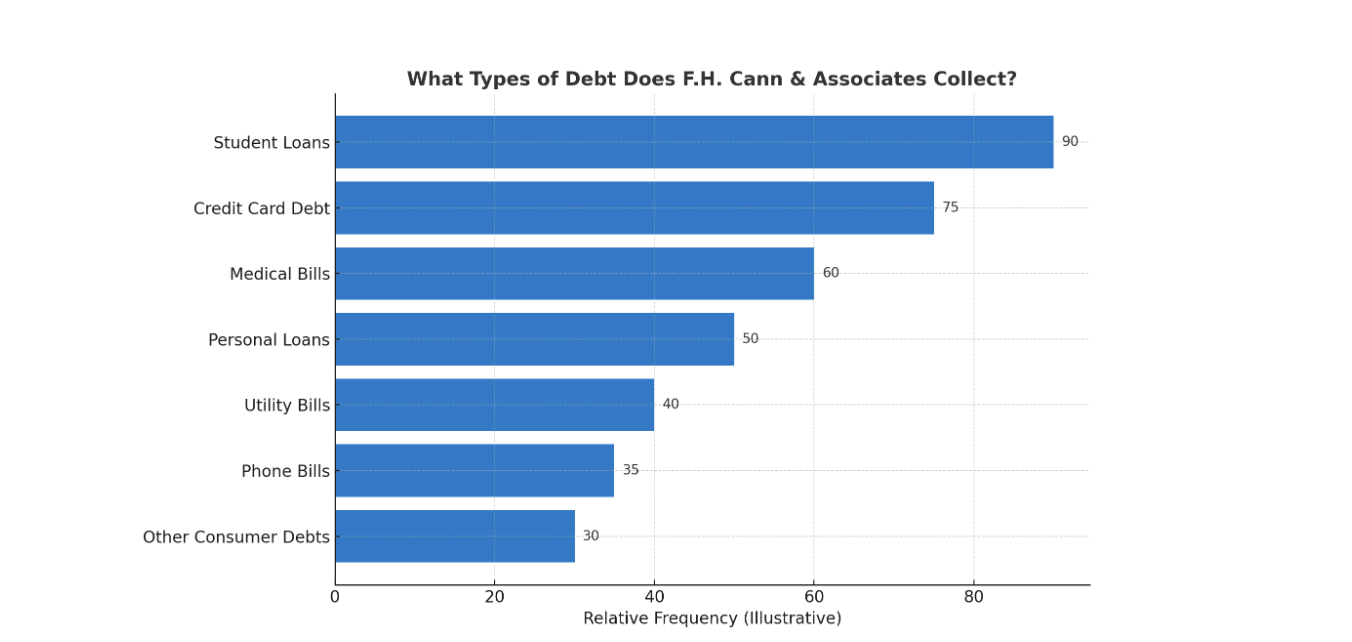

What Types of Debt Does FH Cann Collect?

Fh Cann and Associates collects many different types of debt:

- Student loans

- Credit card debt

- Medical bills

- Personal loans

- Utility bills

- Phone bills

- Other consumer debts

They work as a third-party collector. This means other companies hire them to collect money that people owe.

How to Tell If FH Cann & Associates Is Legit

Fh Cann and Associates is a real, legal debt collection company. Here's how you can tell:

Signs They Are Legitimate

- BBB Accredited: They're accredited by the Better Business Bureau

- Long History: They've been in business since 1999

- Real Address: They have a physical office in Massachusetts

- Proper Licensing: They follow state and federal collection laws

- Website: They have an official website with company information

Red Flags to Watch For

Be careful of scammers pretending to be FH Cann. Real collectors will:

- Give you their full company name

- Provide their address and phone number

- Send written notices about your debt

- Follow collection laws

Fake collectors might:

- Threaten you with jail time

- Demand immediate payment over the phone

- Refuse to give you written information

- Ask for payment with gift cards or wire transfers

- Call from random or blocked numbers

Why Fh Cann and Associates Might Contact You

If FH Cann contacts you, it's because:

- You have an unpaid debt

- Someone with your name or similar information owes money

- You used to live at an address where someone owes money

- There's been a mistake with your information

When they appear on your credit report, it means they're trying to collect on a debt they say you owe.

Common Problems People Have With FH Cann

Based on consumer complaints, people report these issues:

- Too many phone calls

- Calling the wrong person

- Not stopping calls when asked

- Problems with student loan collection

- Difficulty getting debt information

Remember, debt collectors must follow the Fair Debt Collection Practices Act (FDCPA). If they break these rules, you can file complaints.

How to Dispute Fh Cann and Associates

If you think Fh Cann and Associates made a mistake, you can dispute it.

According to Investopedia, consumers have specific rights when dealing with debt collectors, including the right to dispute debts and request validation.

Here are your options:

1. Dispute Directly With FH Cann

Let me share a quick story from one of our clients.

Sarah (not real name) got a letter from FH Cann out of the blue, saying she owed $2,500 for a credit card she swears she never opened. She felt overwhelmed, but instead of panicking, she called their dispute line at (877) 750-9801 and asked for something called “debt validation.” That means she told them: “Prove this debt is mine.”

And guess what?

Within 30 days, they couldn’t provide any proof. No signed agreement, no payment history, nothing. So legally, they had to remove it from her credit report.

You have that same right. You can contact FH Cann directly to dispute:

- A balance that looks way too high

- A debt that isn’t even yours

- Mistakes tied to fraud or identity theft

- Or just to request full documentation. They’re required to provide it

Why Credit Repair Experts Matter

Now, here’s where people usually get stuck.

They don’t know what to say, how to say it, or what to do next. That’s where credit repair experts come in, and where we can save you from a ton of stress and potential damage.

At ASAP Credit Repair, we don’t just send out cookie-cutter letters. We build a real strategy around your situation. We track legal deadlines so you never miss a window. We negotiate directly with collectors and make sure everything is done by the book and in your favor.

Truth is, most people wait too long or send the wrong type of dispute, and that can actually make things worse. But with a professional by your side, you’ll avoid those mistakes and get back on track faster, with a cleaner credit report and a better score to show for it.

2. Dispute With Credit Bureaus

You can also dispute with all three credit bureaus:

- Experian

- Equifax

- TransUnion

Example: Mike found FH Cann on his Experian report for a $1,200 medical bill. He disputed online, explaining he had insurance that covered the bill. Experian investigated and removed the collection after finding the original creditor made an error.

Recommended Read: 5 Easy Steps To File an Effective Experian Dispute

3. What to Include in Your Dispute

When it’s time to dispute a debt from Fh Cann and Associates, don’t just send a vague “this isn’t mine” note and hope for the best. You need to give the credit bureaus or the collector something solid to work with, and show you know your rights.

Here’s what I tell my clients to include in every dispute:

- Your full legal name and current address

This confirms your identity and makes sure they can’t stall you with the old “we couldn’t match you in our system” excuse.

- The account number (if available)

You can usually find this on your credit report or collection letter. If not, describe it as best you can (like: “Collection from F.H. Cann on my Experian report opened in July 2023 for $642”).

- The reason you’re disputing it

Be specific. Are you disputing the balance? The ownership? The account status? For example: “This account is inaccurate, the amount is wrong and I never received validation.”

- Any supporting documentation you have

Think: proof of payment, identity theft affidavit, letters from the original creditor, police reports. Even a simple screenshot from your credit report helps.

- A clear request for validation or deletion

Don’t assume they’ll know what you want. Spell it out: “Please investigate and delete this account from my credit report if it cannot be fully verified under the FCRA.”

I’ve seen firsthand how a strong, well-documented dispute can get results where a generic letter fails. If you want to go deeper, we have a full article dedicated to what should be on your dispute letter. It’s worth the read if you’re serious about getting F.H. Cann off your back.

4. Debt Validation Rights

According to the Consumer Financial Protection Bureau (CFPB), you have 30 days from their first contact to request debt validation. They must prove:

- You owe the debt

- The amount is correct

- They have the right to collect it

Example: When Jennifer got a call from FH Cann about a $800 utility bill, she immediately sent a debt validation letter. FH Cann couldn't prove the debt belonged to her (it was her ex-husband's), so they stopped collection efforts.

5. Keep Records

Save everything:

- Letters they send you

- Records of phone calls

- Your dispute letters

- Responses from credit bureaus

What Happens After You Dispute?

After you dispute:

- Investigation: They have 30 days to investigate

- Response: They must respond with proof or remove the debt

- Credit Report Update: If they can't prove the debt, it gets removed

- Your Rights Continue: You can still file complaints if they violate laws

Settlement and Payment Options

Now let’s talk about handling a valid, collectible debt, meaning no errors, no identity mix-ups, and no statute of limitations issues.

In other words, the debt is legit, and they have the legal right to collect.

At this point, your focus shifts from disputing to minimizing the damage and closing the account on your terms.

Here's how to do that smartly:

Can You Settle With FH Cann & Associates?

Yes, many people settle their debts with FH Cann for less than the full amount. Debt settlement is a common practice where collectors often accept 30-60% of the original debt to close accounts quickly.

Let’s take a look at your options:

1. Negotiate a Pay-for-Delete (PFD)

This is the holy grail of debt resolution. You're offering to pay (often a reduced amount) in exchange for removal of the account from your credit report entirely.

Collectors aren’t required to accept this, but some, including F.H. Cann in past cases, have agreed to it when approached correctly. Start low (30–40% of the balance), be polite but firm, and get everything in writing before you send money.

Tip: Use phrases like “In exchange for payment, I request written confirmation that your company will request deletion of this account from all credit reporting agencies.”

2. Settle for Less Without Deletion

If pay-for-delete is off the table, you can still settle for less. Just know: the account may show as “settled” rather than “paid in full,” which won’t help your score much, but it does stop collection activity and lowers your risk of lawsuits.

Make sure the settlement is in writing and double-check that they won’t come after you for the rest later (yes, that happens).

3. Request a Payment Plan (Last Resort)

If you can’t afford a lump sum, you can request a payment plan. Just beware: unless you get a deletion agreement, the negative account stays on your report, and monthly payments can actually reset the statute of limitations — reopening the window for legal action if you miss a payment.

Only go this route if you’re confident in your ability to pay every installment on time.

Bottom line: your goal isn’t just to pay, it’s to pay smart. Never send money without a paper trail, and always push for terms that protect your credit. If you’re unsure what to offer or how to frame it, get help. These negotiations aren’t one-size-fits-all, and the wrong move can cost you thousands or years of credit damage.

Real Example: Tom owed $3,000 on an old credit card that FH Cann was collecting. He offered $1,500 as a lump sum payment. After some negotiation, they accepted $1,800 (60% of the original debt) and agreed to mark it "paid in full" on his credit report.

Here's what you should know:

- They may accept 30-60% of the original debt

- Get any settlement offer in writing before paying

- Make sure the agreement removes the item from your credit report

- Never give them access to your bank account

Important: Never pay with gift cards, wire transfers, or prepaid cards. These are signs of scams.

How to Stop FH Cann & Associates From Contacting You

Send a Cease and Desist Letter

According to the Federal Trade Commission (FTC), you can legally stop FH Cann from calling you by sending a cease and desist letter.

Real Example: David was getting 5+ calls per day from FH Cann about a debt he was disputing. He sent a certified cease and desist letter on Monday. By Friday, the calls stopped completely. However, the debt remained on his credit report until he successfully disputed it.

Include:

- Your name and address

- Account number (if known)

- Clear statement: "Stop all contact by phone"

- Your signature

- Date

Send it certified mail with return receipt. After they get your letter, they can only contact you to:

- Confirm they will stop calling

- Tell you about legal action they plan to take

What the Cease and Desist Does NOT Do

- It doesn't make the debt go away

- It doesn't stop them from reporting to credit bureaus

- It doesn't prevent them from suing you

- It only stops phone calls and letters

When FH Cann & Associates Might Sue You

According to Investopedia, debt collectors typically sue when it's financially worth it. FH Cann might take you to court if:

- The debt is large (usually over $1,000)

- You ignore them completely

- The debt is still within the statute of limitations

- They think they can collect the money

Example: Robert ignored a $5,000 debt from FH Cann for 8 months. They sued him and won a default judgment because he didn't respond to court papers. His wages were then garnished for the full amount plus court costs.

Important Tips for Dealing With FH Cann

- Don't Ignore Them: According to Forbes, ignoring debt collectors often leads to lawsuits and wage garnishment

- Get Everything in Writing: The FTC recommends getting all agreements in writing before making payments

- Know Your Rights: Learn about the FDCPA from the CFPB website

- Keep Good Records: Save all letters and notes about calls

- Consider Professional Help: A credit repair specialist can help navigate complex situations

Success Story: Karen was overwhelmed by multiple collection accounts, including FH Cann. She hired a credit repair specialist who helped her dispute three incorrect debts and negotiate settlements on two valid ones. Her credit score improved by 127 points in 6 months.

Final Thoughts

FH Cann & Associates is a legitimate debt collector, but that doesn't mean every debt they collect is valid. You have rights under federal law.

If you see them on your credit report:

- Don't panic

- Request debt validation first

- Consider settlement if the debt is valid

- Dispute if something seems wrong

- Send cease and desist to stop calls if needed

- Keep detailed records of everything

- Know your legal rights under the FDCPA

Quick Action Steps:

- Verify the debt - Ask for validation within 30 days

- Check your options - Dispute, settle, or pay in full

- Protect yourself - Never ignore them, but know your rights

- Get help - Consider working with a credit repair specialist

Remember, even legitimate debt collectors make mistakes. It's always worth checking to make sure the debt is really yours and the amount is correct.

Important: If FH Cann violates any collection laws, document everything and consider filing complaints or seeking legal help. You have the right to be treated fairly.

If you need help dealing with FH Cann & Associates or other credit issues, consider working with a credit repair specialist. We know the laws and can help protect your rights while working to improve your credit score.

Have questions about FH Cann & Associates or other items on your credit report? Contact a qualified credit repair specialist for personalized help with your situation.

Disclaimer: This article provides general information about FH Cann & Associates and debt collection practices. We are not affiliated with FH Cann & Associates in any way. All information is for educational purposes only and should not be considered legal advice. Individual situations may vary, and outcomes are not guaranteed. Always verify current company information and policies directly with FH Cann & Associates, as details may change over time.