Hey, you! Yeah, I'm talking to you. Feeling haunted by some forgotten debts lurking in the shadows of your credit report? Don't sweat it. We all make mistakes sometimes. Life gets busy, and bills slip through the cracks. But listen, those scary old debts don't have to keep haunting your credit and holding you back.

Here's the good news: you've totally got options for banishing those pesky problems from your financial history. The first thing you'll want to try is disputing those debts through a credit repair agency. Get 'em to investigate and verify everything is legit. You'd be surprised at how many mistakes happen! If that doesn't do the trick, you can try settling the debts - often for way less than what's owed. Either way, you can send those bad credit ghosts packing. Your credit will be haunt-free in no time. Now go get 'em!

Contents:

How Forgotten Debts End Up on Your Credit Report

Have you ever taken out a loan, credit card, or other line of credit and then forgotten to make payments? It happens more often than you might think. Life gets busy, mail gets misplaced, and debts slip through the cracks. Before you know it, that forgotten bill has been sold to a collection agency and is now dragging down your credit score.

Lack of Communication

The first way forgotten debts end up on your credit report is simply due to a lack of communication. Maybe you moved and forgot to update your address with creditors. Maybe you were going through a difficult life event and bills took a backseat. Regardless of the reason, failing to stay in contact with creditors about payments owed is a surefire way for a debt to end up in collections.

Unpaid Automatic Payments

Another common way forgotten debts surface is when automatic payments are set up, then cancelled for some reason without notifying the creditor. If you had a credit card on auto-pay but then switched banks or accounts and forgot to provide the new details, missed payments can quickly accumulate. Creditors don't care why payments were missed, they just report the delinquency to credit bureaus.

Co-signed Loans

Finally, you may have forgotten about a debt because you co-signed on a loan with someone else. If the other person failed to make payments as agreed but you were still jointly liable, the missed payments can show up on your credit reports, too. It's important to stay on top of the payment status for any debts you co-sign, or risk them becoming forgotten debts that damage your credit.

The good news is that there are steps you can take to remove forgotten debts from your credit reports. Disputing errors, settling with collection agencies, and negotiating pay-for-delete agreements are all strategies that can help erase the negative impacts of unpaid debts you had genuinely forgotten about. With some time and persistence, you can move on from old, forgotten debts and rebuild your credit.

Recommended: How Can I Repair My Credit Quickly: A Fast-Track to Financial Recovery

The Damage Derogatory Debt Can Cause to Your Credit Score

Derogatory debts like the one showing up on your credit report can do some serious damage. These types of debts, especially if left unpaid, can tank your credit score by 100 points or more. Why? Because credit scoring models view people with unpaid collections and charge-offs as high-risk,.

Lower Credit Scores Mean Higher Interest Rates

A lower credit score means you'll pay more for credit cards, auto loans, and mortgages-if you can get approved at all. Lenders see you as risky, so they charge higher rates to offset that risk. The difference between a good and bad credit score can cost thousands extra per year in interest.

Limited Access to Credit

With a low score, many lenders may deny your applications outright. Those that do approve you will likely offer much lower credit limits and higher APRs. You'll struggle to qualify for rewards cards and special financing offers. Bad credit can lock you out of home and auto loans as well.

Impact on Insurance Rates

In many states, insurance companies consider your credit score when determining your premiums. People with bad credit often pay significantly higher rates for auto, home, and life insurance. Some estimates indicate poor credit can raise insurance costs by as much as 50–100% per year.

Difficulty Renting an Apartment

Most landlords check credit reports as part of the rental application process. Unpaid debts and a low score can lead to a rejected application or requirements like a larger security deposit. In a competitive rental market, your application may go straight to the bottom of the pile.

Good Read: Expert Hacks on How to Get Approved for a Rental with Bad Credit

Disputing the item with the credit bureaus is a good first step, as errors often exist. While it may take time, removing derogatory debts can help boost your score and open up more opportunities.

Disputing Inaccurate or Invalid Debts on Your Credit Report

Have you checked your credit report lately and found debts you didn't recognize or thought were paid off years ago? Unfortunately, errors and invalid debts do end up on credit reports, damaging your score and causing headaches. The good news is, you have the right to dispute these inaccuracies and get them corrected.

Disputing a debt on your credit report is actually pretty straightforward. You'll contact either the credit bureau that's reporting the debt (like Equifax, Experian or TransUnion) or the collection agency that's trying to collect the money. Explain in writing that you don't believe the debt is valid or accurate. The credit bureau or collection agency then has 30 days to verify the debt is legit or remove it from your credit report.

Gather Evidence to Support Your Claim

To have the best chance of success, provide copies of any evidence you have that proves the debt is inaccurate or invalid.

Look at things like:

- Cancelled checks showing the debt was paid.

- Correspondence with the original creditor confirming payment.

- Proof that the debt is too old to be reported (older than 7 years).

- Identity theft affidavit if the debt was opened fraudulently.

The more evidence you provide, the more likely the disputed item will be removed. Make copies of everything and submit with your written dispute letter.

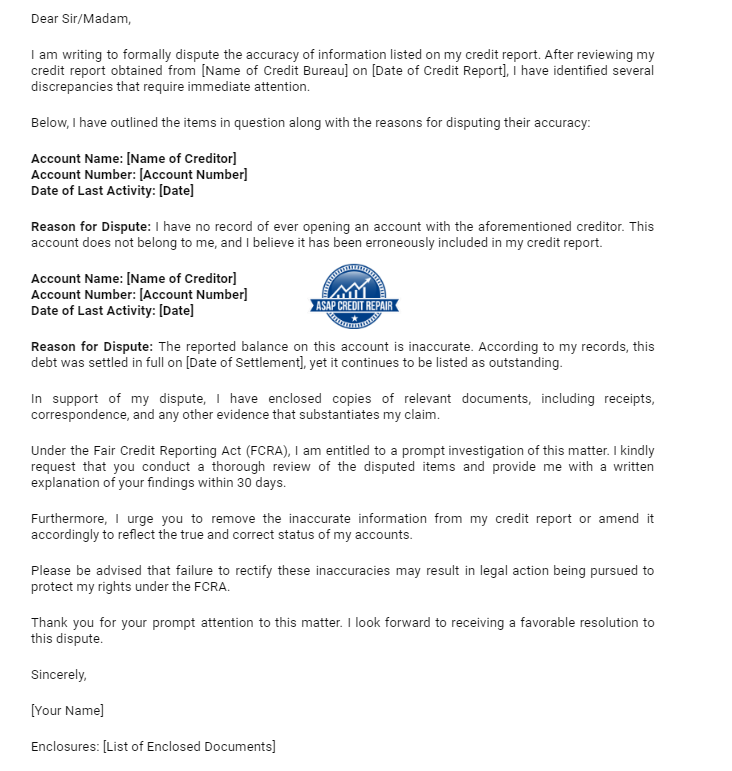

Send a Formal Dispute Letter

Draft a letter stating you are disputing the debt and want it removed from your credit report. Explain specifically why you believe the debt is inaccurate or invalid. Be polite yet firm, and reiterate that according to the Fair Credit Reporting Act, the information must be verified or removed within 30 days. Send the letter via certified mail with return receipt so you have proof it was received.

Disputing debts on your credit report that you don't believe are valid is one of the best ways to start improving your credit. Don't let errors and inaccuracies hold your score down-take action and get them removed so you can get back on track to good financial health. Stay persistent, provide solid evidence to back up your claim, and don't take "no" for an answer. Your credit is worth fighting for!

Look at our sample dispute letter below:

Check out: The Complete Guide to Writing A Winning Dispute Letter

When to Consider Settling Old Debts

So you've disputed that old, unpaid debt that's haunting your credit report to no avail. Now what? In some cases, settling the debt may be your best option to resolve the issue once and for all.

If the debt has been sold to a collection agency, they likely paid pennies on the dollar for the right to collect from you. This means they may be willing to settle for much less than the full amount owed. Contact the agency and let them know you want to settle the debt in exchange for them removing it from your credit reports. Start by offering to pay 30-50% of the balance in one lump sum. Be prepared to negotiate from there.

Many collection agencies are willing to settle because some money is better than no money. They may claim they can't remove it from your credit, but stand firm that a settlement is contingent on deletion. Get any agreement in writing before paying.

If the original creditor still owns the debt, settlement may be trickier but still possible. Explain your situation, take responsibility for the unpaid bill, and ask if they'd consider a settlement. Offer a lump sum of at least 50% to start. Be prepared for them to only agree to mark the debt as "settled" on your credit, not remove it. Take what you can get.

While settling damage has already been done to your score, a settled or deleted derogatory mark is better than an outstanding one. Your score should start to rebound over the next 6-18 months as the settlement ages. Meanwhile, keep paying bills on time and check your credit report regularly to ensure the settlement is properly reflected.

Settling old debts is often a last resort, but it can be necessary to resolve serious delinquencies and move on from past mistakes. If done right, you can settle for less than owed and potentially see the account removed from your credit history, allowing you to get back on the road to good financial health. With time and good habits, you can rebuild your credit even after settlement.

Removing Derogatory Debt Through Credit Repair

So you checked your credit report and found an old, unpaid debt marring your record. The damage has already been done, but the good news is you can take steps to remove this derogatory item and repair your credit.

Dispute the Debt

Disputing the debt with the credit bureaus is your first line of defense. There are a few reasons a debt may not actually be valid or accurate: incorrect information reported, lack of verification, or failure to notify you. File a formal dispute in writing with Equifax, Experian, and TransUnion questioning the validity of the debt. Provide any evidence you have that it's in error. There's a good chance one or more bureaus will remove the debt from your report.

Hire a Credit Repair Service

If disputing doesn't work, consider hiring a credit repair service like ASAP Credit Repair. We are experts at investigating debts and negotiating with creditors and credit bureaus to get derogatory items removed. We know the laws around credit reporting and can re-dispute the debt on your behalf, re-verifying facts and pushing back on the creditor if needed. Credit repair services typically charge a monthly fee, but they can be very effective at cleaning up your credit report. Learn more about ASAP Credit Repair here.

Recommended: What Is Credit Repair Company and What Can They Do For Your Bad Credit

Settle the Debt

If all else fails, you may need to settle the debt to get it removed from your credit. Contact the creditor and offer to settle the debt for less than the full amount owed. Make it clear that you expect the debt to be removed from your credit report once paid. Get the agreement in writing before sending payment. While settling will require you to pay money out of pocket, removing a derogatory debt from your credit report can help your score recover over time.

By taking action, you can dispute, repair, or settle old debts to remove them from your credit report. While it may require patience and persistence, cleaning up your credit history and improving your score will give you more financial freedom and opportunities in the long run. Stay positive.

Don’t Worry About Forgotten Debts Anymore

So there you have it – a comprehensive guide to tackling those pesky forgotten debts that may be haunting your credit report. Whether it's through disputing errors, settling debts, or seeking the assistance of credit repair services, there are viable options available to help you clean up your financial history.

Remember, the journey to repairing your credit may require patience and persistence, but the payoff is well worth it. By taking proactive steps to address these issues, you're not only improving your credit score but also opening up opportunities for better financial health and stability.

So go ahead, take charge of your credit destiny. With determination, the right strategies in place, and the help of ASAP Credit Repair USA, you can banish those haunting debts and pave the way for a brighter financial future. Don't let the ghosts of past mistakes hold you back – you've got the power to rewrite your credit story.