In today's busy world, many people worry about money, especially when they have bad credit.

You've been there. Bills piling up, debt is creeping higher, and credit scores are sinking lower. It's enough to keep you up at night, worry you all day, and generally make your life miserable. Studies show that this kind of stress can really affect your mental and physical health, making you feel more anxious, sad, and even affecting your heart health (APA, 2014). But don't worry, it's totally possible to feel better and get your finances back on track.

But it doesn't have to be like this.

Sure, money troubles can be overwhelming, but you're stronger than your bank account. Start with a few smart money moves and some lifestyle tweaks, and you can get back on track. Don't let past mistakes or a bad credit score get you down. Take control of your finances, starting today. Little steps lead to big changes.

In this guide, we'll give you simple tips and tricks to help you overcome stress caused by bad credit and feel more at ease with your money.

![]()

How Bad Credit Can Affect Your Life

As we grow older, we often become more aware of the far-reaching implications of our financial decisions, particularly when it comes to credit. When we learn how essential having a tier 1 credit score is, we strive to make things better.

Bad credit, in particular, can cast a long shadow over various aspects of our lives, extending beyond simple monetary concerns. Let's explore how bad credit can affect your life in significant ways.

Limited Access to Financial Opportunities:

One of the most immediate impacts of bad credit is the restriction it places on accessing financial opportunities. Whether it's securing a mortgage for your dream home, obtaining a car loan, or even qualifying for a credit card with favorable terms, poor credit history can significantly limit your options. This limitation not only affects your ability to make significant purchases but also hampers your financial flexibility and autonomy.

Recommended: How to Get a Personal Loan With a 500 Credit Score

Higher Borrowing Costs:

Bad credit doesn't just limit your access to credit—it also comes with a hefty price tag. Lenders view individuals with poor credit as higher-risk borrowers, necessitating the imposition of higher interest rates and fees to mitigate potential losses. Consequently, individuals with bad credit end up paying more in interest and financing charges over time, further exacerbating their financial burden.

Strain on Personal Relationships:

Financial stress, often exacerbated by bad credit, can take a toll on personal relationships. Money matters are a leading cause of conflict and tension among couples, with disagreements over finances frequently cited as a primary reason for divorce (Dew & Dakin, 2011). The strain of bad credit can exacerbate these tensions, leading to heightened stress, arguments, and, in severe cases, relationship breakdowns.

Impact on Mental Health:

The pervasive stress and anxiety stemming from bad credit can have profound implications for mental health and well-being. Research has consistently linked financial stress to increased rates of depression, anxiety, and other mental health disorders. The constant worry about debt, bills, and financial insecurity can erode self-esteem, trigger feelings of shame and guilt, and ultimately contribute to a diminished quality of life.

Professional Limitations:

Beyond its effects on personal life, bad credit can also impact professional opportunities and aspirations. Certain industries, particularly those requiring security clearances or financial responsibilities, may conduct credit checks as part of the hiring process. A poor credit history could raise red flags for employers, potentially limiting career advancement opportunities or even resulting in job loss.

It causes constant stress and worry. The consequences of bad credit tend to snowball, creating a cycle of financial anxiety and hardship that's hard to break. You may struggle just to afford basic necessities, let alone save money or pay off debt.

You must be interested with Investing 101: What I Wish I'd Known as a Newbie

![]()

The Psychological Impact of Financial Stress

Financial stress can take a serious toll on your mental health and wellbeing. When money worries become overwhelming, they can trigger anxiety, depression and other psychological issues. The constant pressure of debt, collections and other financial problems can leave you feeling hopeless, helpless and out of control.

Here are some of the main psychological impacts of financial stress:

Anxiety

Having bad credit often means dealing with collectors calling nonstop, the fear of not being able to pay bills, and the worry that you’ll never climb out of debt. In addition, worrying excessively about bills, debt and your financial situation can cause anxiety and panic attacks. You may experience physical symptoms like rapid heartbeat, difficulty sleeping and irritability.

It’s no wonder that financial troubles frequently lead to anxiety and eventually depression. The constant stress can make you feel powerless, hopeless and alone.

Depression

Did you know that Financial problems are a leading cause of depression?

Research has consistently shown a strong correlation between financial stress and depression. According to a study published in the Journal of Family and Economic Issues, financial strain was found to be a significant predictor of depression symptoms among individuals (Conger et al., 2002).

Furthermore, a report by the National Alliance on Mental Illness (NAMI) highlights that financial difficulties, including debt and unemployment, can exacerbate existing mental health conditions or contribute to the development of new ones, such as depression (NAMI, 2020).

These findings underscore the profound impact that financial problems can have on mental well-being, emphasizing the importance of addressing financial stressors to mitigate the risk of depression and other mental health issues.

References:

Conger, R. D., Conger, K. J., Elder Jr, G. H., Lorenz, F. O., Simons, R. L., & Whitbeck, L. B. (2002). A family process model of economic hardship and adjustment of early adolescent boys. Journal of Family and Economic Issues, 23(2), 99-123.

National Alliance on Mental Illness (NAMI). (2020). Financial Assistance. Retrieved from https://www.nami.org/Your-Journey/Individuals-with-Mental-Illness/Finding-Support-Resources/Financial-Assistance

Anger and irritability

When money is tight, even small annoyances can trigger outbursts of anger and frustration. This easily escalates, especially when you are dealing with the long-term consequences of poor credit. Constant financial stress puts you in a heightened state of irritability that impacts your personal and work relationships.

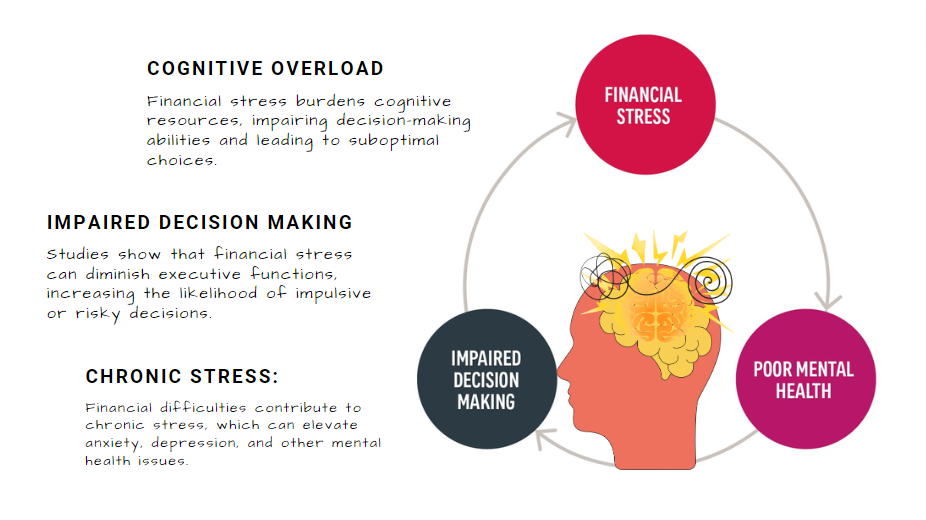

Lower cognitive function

Financial stress, particularly associated with bad credit, imposes a heavy cognitive burden, depleting mental resources essential for various tasks. Research indicates that prolonged financial strain can significantly impair cognitive functions, including memory, decision-making, and self-control.

For instance, a study published in the Journal of Economic Psychology found that individuals experiencing financial stress exhibited poorer performance on cognitive tasks compared to those with lower levels of financial stress (Lindner, Retzler, & von Känel, 2019). Furthermore, chronic financial worries have been linked to structural changes in the brain, particularly in regions responsible for executive functions such as planning and decision-making (Ansell, 2020).

This cognitive depletion due to financial stress can manifest in various aspects of daily life, from struggling to recall important information to making impulsive or irrational decisions regarding finances. Therefore, it's crucial to recognize the cognitive toll of financial stress and take proactive steps to address it.

Relationship Strain

Money problems are a leading cause of arguments and divorce. Financial issues create tension, blame and distrust that place a heavy burden on relationships with family and friends.

Poor Self-Esteem

Bad credit also damages your self-esteem. You may see yourself as incompetent or irresponsible, even if circumstances beyond your control, like medical bills or job losses, contributed to your debt. It’s important to avoid blaming yourself and instead, focus on the actions you can take now to improve your situation.

Trouble Sleeping

Money worries make it difficult to sleep. Your mind races thinking about how you’re going to make payments or what else might go wrong. Lack of sleep then makes your financial and emotional issues seem even more overwhelming. It’s a vicious cycle. Establishing a calming bedtime routine, limiting screen time before bed, and practicing relaxation techniques can help.

The psychological effects of bad credit are significant but the good news is, you can take control of your financial life and ease these stresses. There are always alternatives and solutions, which we’ll talk about later. So don't lose hope! With time and perseverance, you can overcome debt and build the life you want.

![]()

Strategies for Managing the Stress of Bad Credit

Dealing with the stress of bad credit requires a proactive approach and a commitment to regaining financial control.

Here are some effective strategies to help you navigate this challenging situation:

Educate Yourself

Think, be calm, and educate yourself. The first thing to do is try not to panic. Bad credit happens to many people for reasons outside of their control. Take a step back and look at your credit report to understand your full situation. Stay calm—negative emotions will only make the stress worse and prevent you from thinking clearly.

Start by gaining a comprehensive understanding of your current financial situation. Review your credit report to identify any inaccuracies or areas for improvement. Educate yourself about credit scores, debt management strategies, and your rights as a consumer. Knowledge is power, and arming yourself with information will empower you to make informed decisions and take proactive steps towards financial recovery.

Create a Budget

Once you have a handle on your credit issues, make a concrete plan for improving your score over time. Pay down high-interest debts first, then work your way to small balances. If needed, speak to a credit counselor for guidance on setting up a realistic payoff schedule. Having a plan in place will make you feel more in control and ease anxiety.

Developing a realistic budget is essential for managing the stress of bad credit. Take stock of your income, expenses, and debt obligations, and allocate funds accordingly. Prioritize essential expenses such as housing, utilities, and groceries, and identify areas where you can cut back on non-essential spending. By living within your means and sticking to a budget, you can regain a sense of control over your finances and reduce stress.

Communicate with Creditors

Don't be afraid to reach out to your creditors and lenders to discuss your financial situation. Many creditors offer hardship programs or payment arrangements for borrowers experiencing financial difficulties. Explain your circumstances honestly and explore options for reducing interest rates, waiving fees, or restructuring payment plans. Open communication can help alleviate stress and prevent further damage to your credit.

Focus on Debt Repayment

Develop a strategy for tackling your outstanding debts systematically. Consider prioritizing high-interest debts or accounts in collections to minimize interest charges and improve your credit score over time. Explore debt repayment methods such as the snowball or avalanche method, depending on your financial goals and preferences. Celebrate small victories along the way to stay motivated and track your progress towards debt freedom.

Practice Self-Care

Managing the stress of bad credit can take a toll on your mental and emotional well-being. Make self-care a priority by incorporating stress-relief activities into your daily routine. Whether it's meditation, exercise, spending time with loved ones, or pursuing hobbies, find activities that help you relax and recharge. Taking care of your mental health is essential for navigating financial challenges with resilience and positivity.

Don't Obsessively Check Your Score

It's tempting to check your credit score repeatedly to see if it's going up, but this will likely increase feelings of stress and frustration. Limit yourself to checking reports and scores once every few months at most. As long as you're working on your plan, your score will improve over time. Constantly monitoring small fluctuations will only drive you crazy!

Seek Professional Help

If you're feeling overwhelmed or unsure of how to proceed, don't hesitate to seek professional assistance. Work with ASAP Credit Repair! Credit counseling agencies and financial advisors specialize in helping individuals manage debt, improve credit scores, and achieve financial goals. They can provide personalized guidance, negotiate with creditors on your behalf, and offer practical strategies for overcoming bad credit-related stress.

Managing the stress of bad credit requires a combination of education, proactive planning, and self-care. By empowering yourself with knowledge, creating a realistic budget, communicating with creditors, focusing on debt repayment, prioritizing self-care, and seeking professional help when needed, you can effectively navigate the challenges of bad credit and work towards a brighter financial future.

![]()

Financial Stress FAQ: Straightforward Answers to Your Money Concerns

While the road to credit health can be long, staying focused on your goals and maintaining a balanced lifestyle will help make the journey less stressful. Don't lose hope—with time and perseverance, you can overcome the challenges of poor credit. Stay strong and remember that this too shall pass. Here’s to answer your frequently asked questions:

Why is my credit score so low?

There are a few common reasons why your credit score may have taken a hit. Late or missed payments on bills like credit cards, auto loans, or your mortgage are a major culprit. High credit card balances that are close to your limits can also hurt your score. Too many new applications for credit in a short period of time, known as “hard inquiries,” signal risk to lenders and lower your score.

You can also check out my video below about missed and late payments.

How can I improve my credit score?

The good news is, you can take steps to boost your score over time. Make all payments on time going forward. Pay down high credit card balances to keep balances low relative to your limits. Limit new applications for credit. Check your credit report for errors and dispute them. You may also want to consider credit counseling or a debt management plan to help negotiate with creditors.

How long will it take to rebuild my credit?

Rebuilding credit depends on the issues impacting your score. If you only have a few missed payments, your score may start to rebound in 3 to 6 months of on-time payments. Reducing high balances or limiting new applications may provide a quick boost. More serious delinquencies can take longer to recover from, often 12 to 24 months of positive credit behavior. The impact of bankruptcies and foreclosures may take several years to fade. The key is to be patient and consistent.

Should I close unused credit card accounts?

Closing credit card accounts may seem like a good idea when you're trying to regain control of your finances. However, it can actually hurt your score by reducing your available credit and credit utilization ratio. Only close accounts if they charge annual fees you can't afford. Instead, stop using unused cards but keep them open. This maintains your available credit but prevents additional charges. As your score improves, you can reevaluate whether to close any accounts.

Staying on top of your credit and taking steps each month to strengthen it will help ease your financial stress in the long run. Be patient and consistent, ask questions, and don't lose hope! With time and dedication, you can overcome credit challenges.

![]()

Conclusion

Having bad credit doesn't define you or your worth. It's merely a temporary obstacle, a challenge that many have faced and overcome. Don't let financial stress overwhelm you. It's okay to feel frustrated or uncertain, but remember that these feelings are transient. Take it one day at a time, focusing on the small victories and progress you make along the way.

Make a plan, a roadmap to guide you towards financial stability. Set realistic goals and break them down into manageable steps. Seek out resources and advice to help you navigate this journey. And don't forget to lean on your support system—friends, family, or even professional advisors—who can offer guidance, encouragement, and sometimes, just a listening ear.

With some patience and smart money moves, you can get back on track. It won't happen overnight, but every positive choice you make brings you closer to your goals. Stay focused on the future and keep chipping away at improving your credit. Celebrate the progress you've made, no matter how small, and use it as motivation to keep moving forward.

Remember, small steps will lead to big rewards over time. Each payment made, each debt reduced, each responsible financial decision contributes to your journey toward a brighter future. You have the strength and resilience to get through this. Believe in yourself and your ability to create the financial future you want, despite the setbacks.