The Phone Call That Started It All

When Marcus (name changed for privacy) called us, he sounded defeated.

"I've got five collections on my credit report," he said. "I know I messed up. I'm just calling to see if there's anything you can do, but I'm not getting my hopes up."

Five collections. From major creditors:

- Bank of America

- Wells Fargo Bank

- Wells Fargo Card Services

- Amazon (via Synchrony)

- Oportun

His credit score? 492.

He'd been rejected for a car loan three times. Turned down for credit cards. Even apartment applications were coming back with "we've decided to go with another applicant."

Marcus thought he had two options: pay everything off (which he couldn't afford) or wait seven years for them to fall off his report naturally.

He was wrong. There was a third option.

The Truth About Collection Accounts Nobody Tells You

Here's what most people don't understand about collections:

They're almost never 100% accurate.

Think about it. A debt starts with one company, gets sold to a collection agency, maybe sold again, transferred between systems, handled by different people. The original paperwork? Who knows where that is.

By the time it hits your credit report, it's gone through so many hands that errors are practically guaranteed.

We're talking about:

- Wrong dates

- Incorrect amounts

- Missing documentation

- Unverifiable information

- Lack of proper contracts

- No proof of ownership of the debt

And here's the kicker: If they can't prove every single detail is 100% accurate, the Fair Credit Reporting Act says it has to be removed.

Not "updated." Not "noted as disputed."

DELETED.

What We Found When We Looked at Marcus's Report

We pulled Marcus's full credit report and started our investigation.

Every single one of those five collections had problems.

The Bank of America account? The dates didn't match up with the original account opening.

The Wells Fargo accounts? Missing key documentation that's required by law.

The Amazon/Synchrony account? They couldn't verify the original creditor information.

Oportun? Multiple discrepancies in the reporting.

Now, we can't share all the specific details (that's proprietary to our process), but what we can tell you is this: when you know what to look for, you find errors everywhere.

This data confirms that errors and disputes, especially those involving collections, which align with your findings, are very common.

Frequency of Credit Report Errors

Based on federal studies, errors on credit reports are a systemic problem:

40% of all credit report disputes are linked to collections accounts, which highlights why all five of the collection accounts on Marcus's report had problems.

20% of consumers have an error on at least one of their credit reports.

This data demonstrates that finding discrepancies like mismatched dates, missing documentation, and unverified original creditor information is a frequent issue in the credit reporting system.

The 30-Day Process

Here's what we did:

Week 1: Investigation Phase

- Analyzed all five accounts in detail

- Identified specific errors and violations

- Gathered documentation

- Prepared comprehensive dispute letters

Week 2: Filing Disputes

- Filed disputes with all three credit bureaus (Experian, TransUnion, Equifax)

- Challenged the accuracy of each account

- Demanded verification and proof

- Set up our follow-up system

Weeks 3-4: The Waiting Game (That We Don't Really Wait For)

- Credit bureaus have 30 days to investigate

- We followed up relentlessly

- Tracked responses from each bureau

- Prepared for any pushback

The collection agencies and creditors had to prove everything was accurate. Every date. Every dollar amount. Every piece of documentation.

And they couldn't.

The Results (That Honestly Still Blow Us Away)

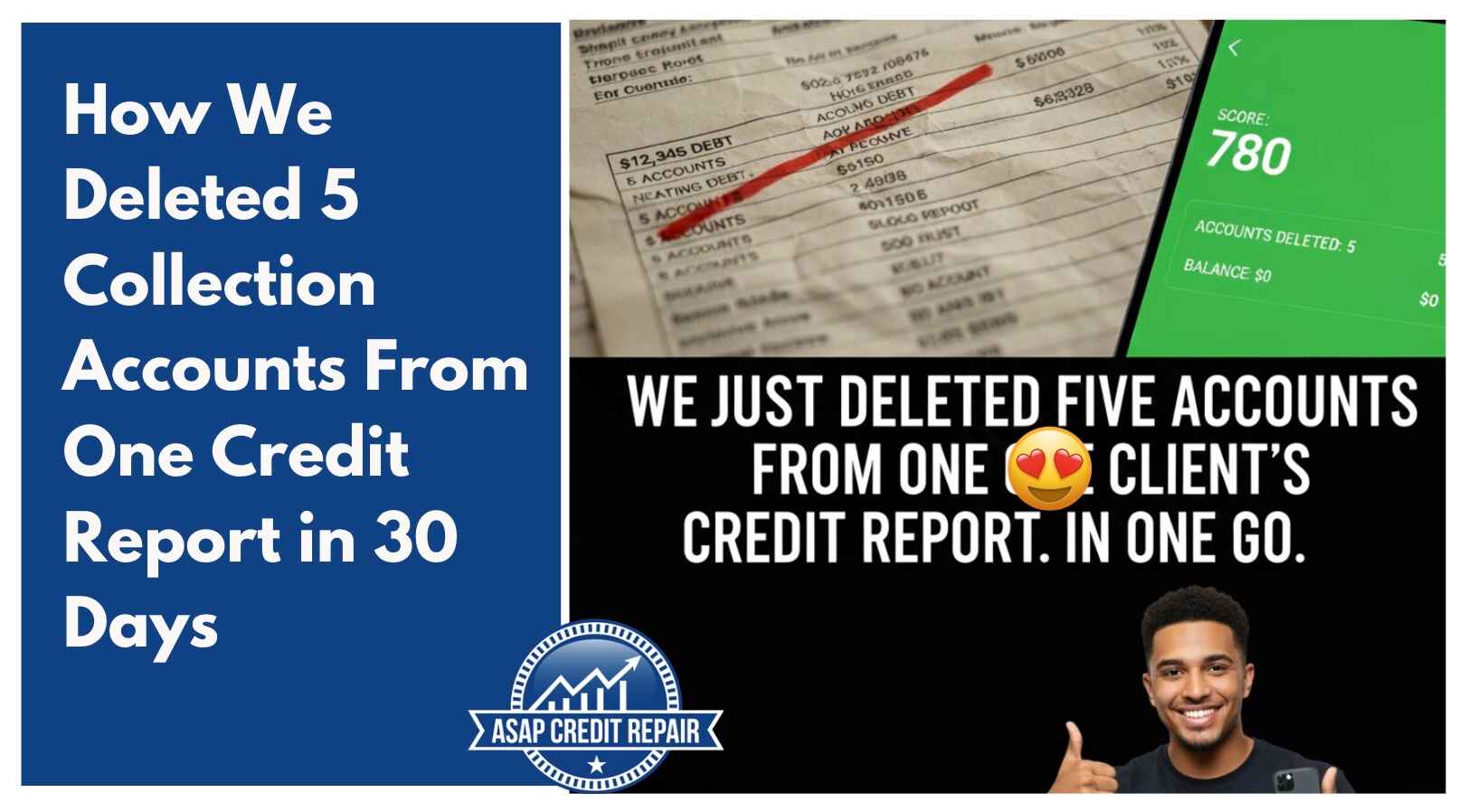

On day 28, we got the investigation results back.

Bank of America: DELETED

Oportun: DELETED

Amazon/Synchrony: DELETED

Wells Fargo Bank: DELETED

Wells Fargo Card Services: DELETED

All five accounts. Removed from all three credit bureaus.

Marcus's credit score? It jumped from 492 to 614.

That's a 122-point increase in less than 30 days.

What Happened Next (The Real Victory)

The number was great. But here's what that number actually meant for Marcus:

Within one week of the deletions:

- He applied for a car loan and got approved

- Interest rate that was actually reasonable (not the predatory rates he'd been quoted before)

- He could finally replace his car that had been dying for two years

Within two weeks:

- Applied for an apartment in a better neighborhood

- Got approved (no more "we've decided to go with another applicant")

- Security deposit was standard, not the inflated amount he'd been asked for previously

Within a month:

- Got his first credit card approval in four years

- $2,500 limit

- Started rebuilding his credit properly

Five deleted accounts didn't just change his credit score. They changed his entire life trajectory.

"But Don't Collections Fall Off After 7 Years Anyway?"

Sure. Eventually.

But let's do the math on what waiting costs you:

Marcus was 32 when he called us. His oldest collection was three years old. That means he would've had to wait another four years minimum for these to age off his report.

Four years of:

- Being denied for loans and credit cards

- Paying higher interest rates on everything

- Being rejected for apartments

- Missing opportunities that require good credit

- Watching his peers get ahead while he's stuck

Or... one month with us and it's all gone.

Which would you choose?

Why Most People Don't Know This Is Possible

The collection industry doesn't exactly advertise that their reporting is full of errors.

Credit bureaus don't send you letters saying "Hey, you should probably dispute these because they might not be accurate."

And most people just accept what's on their credit report as permanent truth.

But it's not.

The Fair Credit Reporting Act exists specifically to protect consumers from inaccurate reporting. You have the legal right to challenge anything on your report. And if it can't be verified as 100% accurate, it must be removed.

The problem is that most people don't know:

- What to look for

- How to challenge it properly

- What documentation to request

- How to follow up effectively

- What to do if the bureaus push back

That's where we come in.

The Accounts We've Successfully Deleted

Marcus isn't unique. We do this all the time.

We've successfully removed collections from:

- Major banks: Chase, Bank of America, Wells Fargo, Capital One, Citibank

- Credit card companies: Discover, American Express, Synchrony, Credit One

- Medical bills: From hospitals, doctors, clinics

- Utility companies: Phone bills, electric, cable/internet

- Auto loans: Both original lenders and collection agencies

- Personal loans: Various lenders and debt buyers

- Retail accounts: Store cards, buy-now-pay-later accounts

If it's on your credit report and it has errors (which most do), we can challenge it.

What You Need to Know If You Have Collections

If you're reading this and you have collection accounts destroying your credit, here's what you should understand:

1. Don't Ignore Them Hoping they'll go away doesn't work. They'll sit there for seven years from the date of first delinquency, destroying your score the entire time.

2. Don't Just Pay Them Paying a collection doesn't remove it from your report. It just changes the status from "unpaid collection" to "paid collection." Still hurts your score. Still shows up for seven years.

3. Don't Try to Negotiate "Pay for Delete" This rarely works, most legitimate collection agencies won't do it, and even if they agree, there's no guarantee they'll actually remove it.

4. Do Challenge Their Accuracy This is your legal right. If they can't verify everything is accurate, it must be deleted. This is the law.

5. Do Get Professional Help Credit repair isn't impossible to do yourself, but knowing exactly what to look for, how to phrase disputes, what documentation to request, and how to follow up effectively makes a massive difference in success rates.

How Much Did This Cost Marcus?

This is usually the next question we get.

Marcus paid our standard fee for credit repair services. The exact amount depends on the number of accounts and complexity, but here's how he looked at it:

Cost of waiting 4+ years for collections to fall off:

- Denied car loans (or predatory interest rates)

- Higher insurance premiums

- Apartment rejections or higher deposits

- No access to credit cards or favorable terms

- Missed opportunities

Cost of working with us:

- One month

- One fee

- Five deletions

- 122-point score increase

- Life back on track

When you frame it that way, the decision becomes pretty obvious.

Your Next Steps

If you have collections on your credit report, here's what we recommend:

Step 1: Pull your credit reports Get them from all three bureaus. You're entitled to free reports at AnnualCreditReport.com.

Step 2: Count your collections How many do you have? From which creditors? What are the dates and amounts?

Step 3: Stop accepting them as permanent Just because it's on your report doesn't mean it's accurate. Just because it's a big bank's name doesn't mean they have proper documentation.

Step 4: Get a professional review We offer free credit report reviews. We'll look at your specific situation and tell you exactly what we can remove and what kind of score increase you can expect.

No sales pitch. No pressure. Just honest analysis of your situation.

Ready to See Your Own Deletion Letter?

Marcus went from five collections and a 492 credit score to a clean report and 614 score in 30 days.

What could your credit look like in 30 days?

Contact ASAP Credit Repair today for your free credit report review.

We'll tell you exactly how many accounts we can remove and what your life could look like after.

Because waiting seven years is ridiculous when we can fix it in weeks.

ASAP Credit Repair - Your score fixed. ASAP.

Individual results vary based on specific circumstances. We dispute inaccurate, unverifiable, and unfair items as permitted under the Fair Credit Reporting Act. Marcus is a real client (name changed for privacy) and the results shown are from an actual case completed in September 2025.