Medical Debt & Your Credit

Medical debt can stay on your credit report for up to 7 years, but it doesn’t always have to. If the debt is inaccurate, unverified, or possibly fraudulent, you can legally challenge and remove it early by validating the debt, disputing errors, and reporting fraud when needed.

This guide is for you if:

- You have unpaid medical bills in collections

- You’re seeing unknown medical debts on your credit report

- Your score dropped due to a hospital bill

- You want to remove medical debt early

How Long Does Medical Debt Stay on Your Credit Report?

Medical debt stays on your credit report for 7 years from the date of your first missed payment.

But there are exceptions: debts under $500 won't be reported, and if insurance pays within a year, it won't appear at all.

How to Spot Fake Medical Debts

Watch out for these warning signs:

- Debt appears from a company you never heard of

- Amount doesn't match any bill you remember

- No date of service provided

- Collector can't explain what treatment the bill covers

It’s important to know this because about 20% of medical debts in collections contain errors or are completely fraudulent.

If you notice any of these red flags, don’t ignore them.

Medical Collections Timeline Breakdown

Medical debt follows the same 7-year rule as other debts, BUT there's a catch most people don't know about.

The 7 years starts from your first missed payment, not when the debt went to collections.

Here's what credit repair experts know that most websites won't tell you:

- 0-180 Days: Medical debt rarely shows up on credit reports during this period. Most hospitals and doctors don't report to credit bureaus directly.

- 180+ Days: Debt gets sold to collections. This is when it hits your credit report and damages your score.

- 365+ Days: Debt often gets sold again to a different collector. Each sale can create a NEW entry on your report.

- 7 Years: Debt must be removed from your credit report.

The $500 Medical Debt Rule (Game Changer for 2024)

Since July 1, 2022, the three major credit bureaus, Experian, Equifax, and TransUnion stopped including medical collections under $500 on consumer credit reports. It had a full blown effect last year. This change was designed to reduce the financial harm caused by small, often unexpected medical bills and gave millions of Americans immediate relief.

If you have a single unpaid medical bill in collections that’s under $500, it should no longer appear on your credit report.

This means it won’t affect your credit score, your ability to qualify for loans, or your overall creditworthiness.

Why This Rule Matters

In the past, even a small unpaid co-pay or missed insurance adjustment could send a bill to collections and damage your credit. Many of these balances were due to:

- Delays or mistakes by insurance companies

- Surprise billing after emergency room visits

- Miscommunication between providers and patients

This new rule provides a buffer, helping consumers avoid long-term credit damage for balances that often weren’t their fault to begin with.

What Is Bundling in Medical Collections?

What many people don’t realize is that multiple small medical debts can be combined, or "bundled", into one larger account. This is if they’re handled by the same collection agency.

Once bundled, the total balance can exceed $500, making it eligible to appear on your credit report, even if each individual bill is under the limit.

For example:

- $200 emergency room visit

- $150 lab test

- $250 imaging fee

If all three are turned over to the same collector, say for example, Wakefield And Associates. They can be grouped into a $600 collection. That balance will show up on your report, even though each bill on its own wouldn’t qualify under the $500 rule.

This practice is legal, and many collection agencies do it to bypass the reporting limit.

What You Can Do About It

If you believe your medical debt is being unfairly bundled, here are steps you can take:

1. Request an Itemized Breakdown

Ask the collection agency to provide a detailed list of charges and dates. Verify that all debts are actually yours and haven't been combined incorrectly.

2. Check for Duplicate or Paid Items

Sometimes, bundled accounts include charges that have already been paid by insurance or were billed in error. If so, you can dispute the total amount.

3. Negotiate to Reduce the Balance

If the bundled amount is just over $500, offer a partial payment to bring it below the threshold. Once it falls under the limit, request that the collection be removed from your credit report.

4. Dispute the Entry with Credit Bureaus

If the bundled account appears inaccurate, you can file a formal dispute with Experian, Equifax, and TransUnion. Be sure to include documentation that supports your claim.

Important Note: This Only Applies to Medical Debt

The $500 rule only applies to medical collections. It does not affect credit card debt, utility bills, personal loans, or any other type of collections. Only medical-related debt that went to collections falls under this rule.

Pro Tip: If you have multiple small medical debts with one collector, they might bundle them together.

A $200 ER bill + $350 lab fee = $550 total, which WILL show up on your report.

Medical Debt vs Regular Debt: Why It's Different

Medical debt gets special treatment that most people don't know about:

Insurance Payment Grace Period

- Medical debt won't appear on credit reports for 1 full year after insurance pays it

- This gives you time to dispute billing errors with insurance companies

- Regular debt can hit your report in just 30-90 days

Lower Credit Score Impact

- Medical debt hurts your score less than credit card debt

- FICO 9 and VantageScore 4.0 weigh medical debt lighter

- But older scoring models (still used by many lenders) treat it the same

Can Medical Debt Be Deleted Early?

Yes, there are several legal and strategic ways to shorten the 7-year reporting period for medical debt. Meaning, you can potentially remove the debt from your credit report before the full 7 years pass.

Here are the most effective ways to do that:

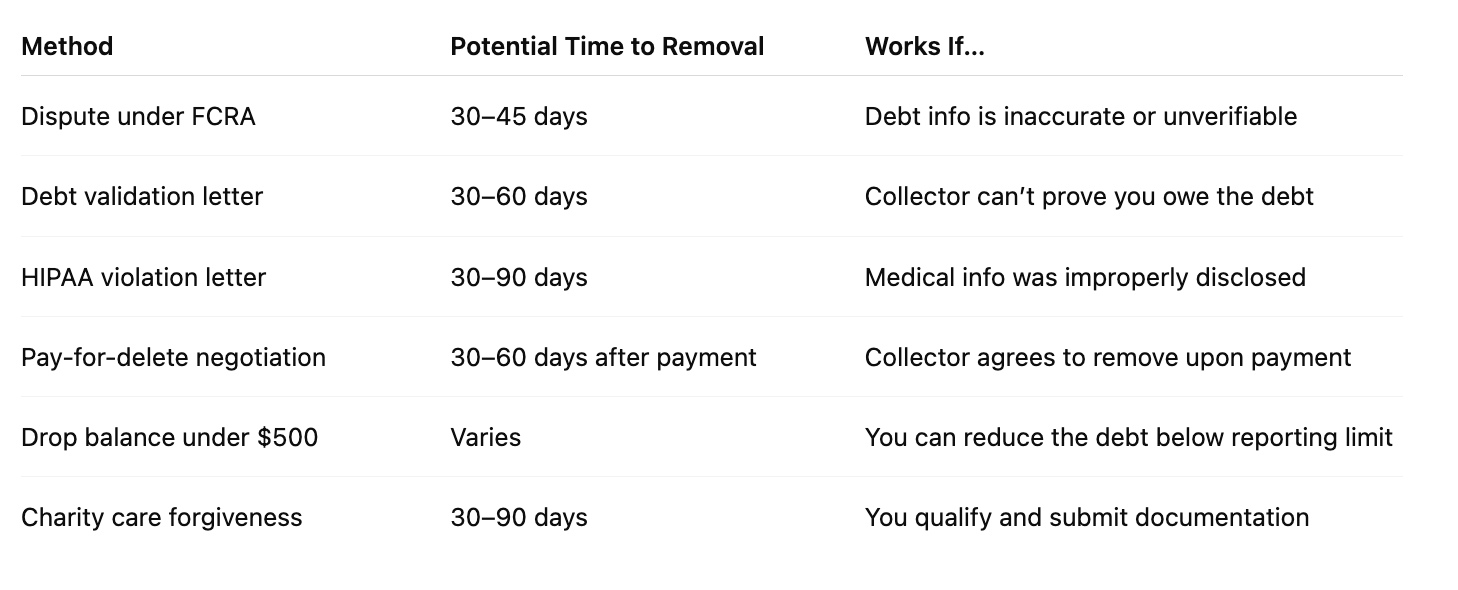

1. Dispute the Debt (Under FCRA)

If the debt contains any incorrect information, such as wrong amount, wrong date, or inaccurate medical billing, you can dispute it under the Fair Credit Reporting Act (FCRA).

Challenge the collector to prove:

- Insurance was billed correctly

- All available insurance benefits were used

- The debt amount is accurate after insurance adjustments

If the collector or credit bureau can't verify the debt within 30 days, they must remove it immediately.

Common dispute triggers:

- Debt amount is wrong

- Date of service is inaccurate

- Insurance wasn’t applied properly

- Debt doesn’t belong to you

2. Send a Debt Validation Letter (Within 30 Days of Contact)

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request proof that:

- The collector legally owns the debt

- The amount is accurate

- You actually owe it

Ask the collector to provide the original signed agreement between you and the hospital/doctor. Medical debts often can't produce this document because there was no signed contract - just implied consent for treatment.

Even if you're past the 30-day dispute window or the debt is valid, it's still worth trying.

Medical debt is the most forgiving type of negative item on your credit report.

Related Read: Understanding IRS Tax Deductions for Medical Expenses

3. Use the HIPAA Violation Strategy

The HIPAA Violation Letter

If a debt collector discloses medical information (such as your diagnosis, treatment, or provider name) to unauthorized parties, they may have violated HIPAA privacy laws.

You can send a HIPAA violation letter, which pressures the collector to remove the debt to avoid legal trouble.

What to look for:

- Collector mentions your specific medical condition

- They discuss treatment details

- They share info with family members without consent

This method is often used by credit repair professionals to get early removals.

4. Negotiate a “Pay-for-Delete” Agreement

If the debt is valid and recent, you can offer to pay in exchange for deletion, known as a pay-for-delete deal.

Medical Debt Negotiation Scripts That Work

For Hospitals (Before Collections)

"I want to pay this bill, but I need to understand if insurance was billed correctly. Can you provide an itemized statement and proof that all my insurance benefits were applied?"

For Collectors

"I'm disputing this debt under HIPAA regulations. Please provide validation that shows you have legal authority to collect this debt and that no protected health information was improperly shared."

Important: Get the agreement in writing before paying. Not all collectors will agree, but many medical debt collectors are more flexible than credit card or loan collectors.

5. Use the $500 Rule to Trigger Removal

If the total debt is just over $500, you can try to:

- Negotiate a partial payment to bring it under $500

- Then dispute it with the credit bureaus, since debts under $500 are no longer supposed to be reported (as of July 2022)

6. Apply for Hospital Charity Care or Hardship Forgiveness

Many hospitals have charity care programs that can reduce or eliminate bills. Write a hardship letter explaining:

- Your income situation

- Medical condition impact on work

- Other financial obligations

If approved:

- Your medical debt will be partially or fully forgiven

- You can then request deletion from the collector or dispute it with documentation

Success Rate: About 60% of people qualify for some form of medical debt forgiveness.

You Can Remove Medical Debt Early

Frequently Asked Questions About Medical Debt

Does paying off medical debt remove it from your credit report?

No, paying off medical debt does not automatically remove it from your credit report. The paid debt will remain for 7 years but show as "paid" or "satisfied." To get it completely removed, you need to negotiate a "pay for delete" agreement in writing before making payment, or wait for it to fall off after 7 years.

Can medical debt be removed before 7 years?

Yes, medical debt can often be removed early through several strategies: HIPAA violation disputes (if collectors shared protected health information), insurance verification challenges (forcing collectors to prove insurance was handled correctly), or debt validation requests. Many medical debts contain errors that make them removable under the Fair Credit Reporting Act.

Do hospitals report medical debt to credit bureaus?

No, hospitals and doctors' offices typically don't report directly to credit bureaus. It's usually the debt collection agencies that report after 180+ days. This is why medical debt often doesn't appear on credit reports immediately - unlike credit card debt that can show up in 30-90 days.

What if my medical debt was sent to collections by mistake?

You can dispute it and demand validation under the Fair Debt Collection Practices Act. Send a debt validation letter within 30 days of first contact asking the collector to prove you owe the debt, the amount is correct, and they have legal authority to collect. If it's inaccurate or they can't validate it, you can get it removed under the Fair Credit Reporting Act.

Credit Score Recovery Timeline

Once medical debt is removed from your credit report:

- 30 days: Minor score improvement (5-10 points)

- 60 days: Moderate improvement (15-25 points)

- 90+ days: Maximum improvement (30-50+ points)

Medical debt removal often has a bigger impact than people expect because it:

- Lowers your debt-to-income ratio

- Removes negative payment history

- Reduces total number of accounts in collections

Preventing Future Medical Debt Problems

Removing inaccurate medical debt is only part of the solution. The bigger step is making sure you don’t get hit with surprise bills again. That’s where the Vital110 Program can help.

With $0 copays on primary care, virtual urgent care 24/7, free labs and prescriptions, plus tools like a Hospital Bill Eraser, Vital110 makes healthcare more affordable and predictable. It even covers your spouse and kids up to age 26. By cutting costs before they turn into collections, you protect both your health and your credit score. Here's what to remember:

Before Treatment

- Always ask about charity care programs

- Request cost estimates upfront

- Verify your insurance coverage

After Treatment

- Review all bills carefully

- Compare bills to insurance EOB statements

- Don't ignore bills - contact the billing department immediately

Emergency Situations

- Even in emergencies, ask about payment plans

- Request financial hardship applications

- Don't sign blank forms or financial agreements

The Bottom Line

Medical debt doesn't have to ruin your credit for 7 years. With the right knowledge and strategies, most medical debt can be removed, reduced, or negotiated away.

The solution is acting fast and knowing your rights under HIPAA, the Fair Credit Reporting Act, and the Fair Debt Collection Practices Act.

Remember THAT medical debt collectors are often more willing to negotiate than regular debt collectors because they know medical debt is viewed differently by courts and credit scoring models.