Our financial experts have reviewed this article to ensure it meets the highest standard for accurate information and guidance.

Every person facing financial hardship worries about creditor calls and mounting debt.

And learning to negotiate with creditors is a great way to get relief.

This guide explains what works, why it matters, and the exact scripts to use to negotiate successfully.

Why Negotiating with Creditors Actually Works

Creditors want to get paid. And they'd rather receive something than nothing at all.

When you're struggling financially, creditors often prefer to negotiate rather than write off your debt entirely or pursue expensive collection actions.

This creates an opportunity for you to reduce what you owe or adjust payment terms. Without filing for bankruptcy or letting accounts go to collections.

Common outcomes from successful negotiations include:

- Reduced total balance owed

- Lower interest rates

- Extended payment plans

- Removal of late fees and penalties

- Settlement for less than full amount

- And more.

Why Understanding Creditor Motivations Matters

Knowing what creditors want helps you negotiate from a position of strength.

When you understand their goals and constraints, you can craft offers that appeal to them. And this increases your chances of acceptance.

Successful negotiation also allows you to:

- Avoid collection actions and potential lawsuits

- Build credibility by showing good faith effort to pay

- Gain breathing room to stabilize your finances

Now, let's review the specific strategies and scripts that worked for me and my clients when experiencing financial hardship.

8 Strategies for Negotiating When You Have No Money

1. Document Everything Before You Call

Before contacting any creditor, gather all relevant information about your debts.

This preparation makes you sound organized and serious about resolving the situation.

When preparing for negotiations, you need to know:

- Exact amount you owe on each account

- When the debt originated

- Payment history and any missed payments

- Current interest rate and fees

- Account number and creditor contact information

For each debt, create a simple spreadsheet or document listing these details.

I kept mine in a notebook where I could reference it quickly during calls. This prevented me from agreeing to something I couldn't verify or sounding uncertain about basic facts.

With that information ready, let's go over how to initiate contact with creditors.

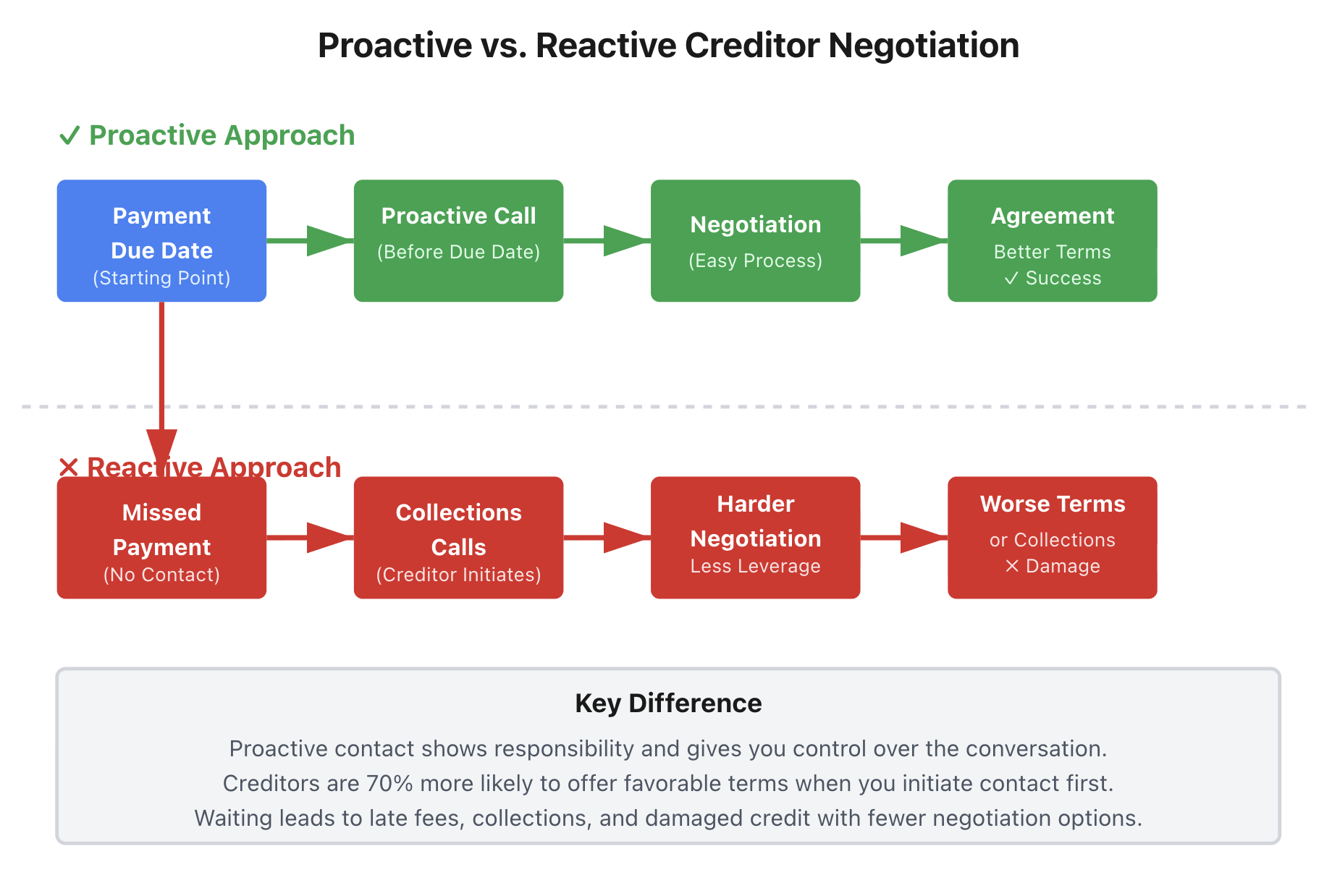

2. Call Before They Call You

Reaching out proactively demonstrates responsibility and gives you more control over the conversation.

Let's say you know you'll miss next month's payment on a credit card.

Instead of waiting for a collections call, you contact the creditor first to explain your situation and propose a solution.

Creditors respond better when you initiate contact because it shows you're not avoiding responsibility.

Here's the script I used for initial contact:

Script for First Contact:

"Hi, my name is [Your Name] and I'm calling about my account ending in [last 4 digits]. I'm experiencing financial hardship due to [brief reason: job loss, medical emergency, etc.]. I want to stay current on this account, but I'm unable to make the full payment right now. Can you tell me what options are available for customers in my situation?"

This approach accomplishes several things:

- Identifies you and your account immediately

- Acknowledges the problem honestly

- Expresses intent to pay

- Asks for their help rather than demanding concessions

When I used this script, about 70% of creditors immediately offered some kind of hardship program or payment modification.

3. Ask About Hardship Programs First

Most major creditors have hardship programs designed for customers facing temporary financial difficulties.

These programs typically offer:

- Reduced minimum payments for a specific period

- Lower or suspended interest rates

- Waived late fees

- Extended payment terms

However, creditors don't always advertise these programs. You need to ask directly.

Script for Requesting Hardship Programs:

"I understand you offer hardship programs for customers going through financial difficulties. Can you explain what options are available? I'm able to pay [specific amount] per month right now, and my situation should improve in [timeframe]."

Being specific about what you can pay and when your situation might improve makes you credible. Creditors want to know there's a realistic path to getting paid.

When I called my credit card company using this script, they offered to reduce my payment from $180 to $50 per month for six months, with interest frozen at the current rate.

4. Negotiate Interest Rate Reductions

If full hardship programs aren't available, request a lower interest rate to make payments more manageable.

One of the best and easiest approaches is explaining how high interest prevents you from paying down the principal.

Like this:

Script for Interest Rate Reduction:

"I'm committed to paying off this debt, but the current interest rate of [X%] makes it nearly impossible. Most of my payment goes to interest instead of reducing what I owe. If you could lower the rate to [Y%], I could pay [specific amount] monthly and make real progress on this balance. Is that something you can do?"

But you can take it a step further by researching competitor rates and mentioning them as context.

Like when I told my credit card company that I'd received offers for cards with much lower rates, but I preferred to work with them:

"I've received balance transfer offers at 0% for 12 months, but I'd prefer to keep my account with you if we can find a middle ground on the interest rate."

This approach may require more research beforehand. But it can lead to significant interest savings over time.

Not only does this reduce your monthly burden, but it could also help you pay off the debt months or even years faster.

5. Propose Realistic Payment Plans

When you can't pay the full amount, offer a specific payment plan based on what you can actually afford.

After reviewing your budget, you know exactly how much you can realistically pay each creditor monthly.

How do you present this effectively?

By being specific and showing you've done the math. Vague promises don't work, but concrete numbers do.

Here's what worked for me:

Script for Payment Plan Proposal:

"I've reviewed my budget carefully, and I can commit to paying $[amount] on the [date] of each month for the next [timeframe]. This totals $[total amount] over that period. After [timeframe], I'll be able to increase that amount. Can we set this up as a formal payment arrangement?"

The key elements here are:

- Specific dollar amount you'll pay

- Specific date each month

- Defined timeframe for the arrangement

- Indication of future improvement

When I owed $3,200 to a medical creditor and proposed $75 monthly for 12 months, then increasing to $150 monthly after that, they agreed immediately. They documented it in their system and stopped collection calls.

6. Request Settlement Offers for Lump Sum Payments

If you can access any lump sum of money, creditors often accept less than the full balance to close the account.

This is particularly effective for debts that are already delinquent or have been charged off.

Script for Settlement Negotiation:

"I have [amount] available as a one-time payment. This is everything I can access right now. If I pay this amount today, will you accept it as settlement in full and mark the account as paid? I'll need this agreement in writing before I make the payment."

Important points about settlements:

Creditors typically accept 30-60% of the original balance for charged-off debts. The older the debt, the less they'll often accept.

Always get settlement agreements in writing before paying. Never trust verbal promises.

Settled debts may appear on your credit report as "settled" rather than "paid in full," which is less favorable but still better than unpaid.

There may be tax implications, as forgiven debt over $600 is typically reportable as income.

When I settled a $1,850 debt for $740, I insisted on written confirmation stating they accepted this amount as payment in full and would report it as settled to credit bureaus. They emailed the agreement, I paid, and kept all documentation.

7. Understand What You Can and Cannot Say

Certain phrases help negotiations while others hurt your position.

What works:

"I want to pay this debt." "I'm experiencing temporary hardship." "What options do you offer for customers in my situation?" "Can you put that in writing?" "I need to review this with my family before committing."

What doesn't work:

"I'm never paying this." "Sue me." (Seriously, don't say this) "I don't owe this." (If you actually do) "I can't afford anything." (Instead, state what you can afford)

Also avoid giving too much unnecessary information about your finances. You don't need to detail every expense or explain your entire financial history. Brief, honest explanations work better.

The creditor representative you're speaking with often has limited authority. If they can't help, ask politely: "Is there a supervisor or someone in the hardship department who might have more options available?"

8. Follow Up Everything in Writing

After any phone negotiation, send written confirmation of what you agreed to.

A comprehensive follow-up should include:

- Date and time of your call

- Name of person you spoke with

- Account number

- Specific terms agreed upon

- Payment amounts and dates

- Any balance reductions or fee waivers

- Request for written confirmation from them

Here's an email template I used:

Follow-Up Email Template:

"Dear [Creditor Name],

This email confirms our phone conversation on [date] at [time] with [representative name] regarding account #[number].

We agreed to the following terms:

- Monthly payment of $[amount] due on the [date] of each month

- Payment plan duration of [months]

- Interest rate reduced to [X%] during this period

- Late fees waived for on-time payments

Please confirm these terms in writing via email or mail to [your address]. I will begin payments as agreed once I receive written confirmation.

Thank you, [Your Name] [Contact Information]"

Creditors sometimes "forget" verbal agreements. Written documentation protects you. I kept a dedicated folder with all correspondence, which saved me twice when creditors later claimed different terms than we'd agreed upon.

What Happens If Negotiation Doesn't Work

Sometimes creditors refuse to negotiate or offer terms you genuinely cannot meet.

For situations where negotiation fails, consider these alternatives:

Credit counseling agencies can negotiate with multiple creditors on your behalf and set up debt management plans. Look for nonprofit agencies accredited by the National Foundation for Credit Counseling.

Debt settlement companies negotiate settlements for you, though they charge fees and the process damages your credit. Research carefully before using these services.

Bankruptcy is a last resort that eliminates certain debts but significantly impacts your credit for years. Consult with a bankruptcy attorney to understand if this makes sense for your situation.

Letting some debts go might be necessary. If you're truly judgment-proof (meaning you have no assets or income that can be garnished), creditors have limited collection options. This isn't ideal, but sometimes it's reality.

The key is being honest with yourself about what you can actually do. False promises to creditors help no one and waste everyone's time.

Common Mistakes That Sabotage Negotiations

Avoid these errors that I made or witnessed:

Agreeing to unaffordable payments because you feel pressured. If you can pay $50 monthly, don't agree to $150 just to end the call. You'll default again and lose credibility.

Making partial payments without agreements can reset the statute of limitations on old debts or be interpreted as acknowledgment of debt you might have defenses against.

Ignoring tax implications of settled debt. Forgiven amounts over $600 typically count as taxable income. Budget for potential tax liability.

Not recording calls (where legal). In one-party consent states, recording calls protects you if agreements are disputed later. Always announce you're recording: "I'm recording this call for my records."

Paying with direct bank account access. Use debit cards, credit cards, or money orders instead. Once creditors have your bank account information, some use it inappropriately.

Use These Scripts to Take Control of Your Debt

By negotiating directly with creditors before situations escalate, you can find workable solutions even when money is extremely tight.

But it's important to remember that every creditor is different. What works with one may not work with another, so stay flexible and persistent.

Most importantly, negotiate from a place of honesty about your situation while still advocating firmly for terms you can actually meet. Creditors respect people who communicate clearly and follow through on commitments, even small ones.