Welcome back to ASAP Credit repair blog! Joe here, and today we're talking about something many of you have asked about, AssetCare LLC showing up on your credit report.

If you've seen this name and wondered "Who is this company and why are they on my credit?", stick around.

We'll cover everything you need to know.

What is AssetCare LLC?

Let's start with the basics.

AssetCare LLC is a debt collection company that purchases charged-off debts from original creditors at pennies on the dollar (typically 3-7 cents per dollar of debt value). They specialize in acquiring portfolios of consumer debt including credit cards, medical bills, and personal loans that are typically 6 months to several years old.

Key Corporate Details

- Founded: 2016 (relatively new in the debt collection space)

- Location: Sherman, Texas

- Primary Address: AssetCare LLC Dept. 0540 P.O. Box 120540 Dallas, TX 75312-0540

- Physical Address: 2222 TEXOMA PY 180 SHERMAN, Texas 75090

- Phone Numbers: 888-993-3596 (automated payment system), 888-993-3604 (speak to specialists)

- Alternative Phone: 888-993-3605

- NMLS License: NMLS number: 1559262

AssetCare Business Structure and Operations

- DBA Names: This debt collection agency also does business under the name of "CF Medical VI, LLC"

- Specialization: AssetCare is a receivables management company that is dedicated exclusively to medical accounts

- BBB Status: Not BBB Accredited. Collections Agencies in Sherman, TX

- BBB Rating: The agency operates to the standard of a B- rating

Known Violation Patterns

It appears as though there are a variety of different complaints against AssetCare LLC alleging violations of the Fair Debt Collection Practices Act (FDCPA) such as falsifying debt and failing to contact consumers regarding debt.

Common Complaint Patterns:

- Putting false information on my credit history

- CFPB prohibit companies to place unpaid medical debt on consumer credit reports

- Medical debt reporting violations

- Inaccurate debt validation

Financial Impact Potential

You could win $1,000 per violation, so when a collection agency chases you for money they cannot legally collect, they may end up having to pay you instead.

Why is AssetCare LLC on My Credit Report?

Good question! AssetCare shows up on your credit report when they report your debt to the credit companies. This usually happens when:

- You had an old debt that got sold to them

- They're trying to collect money from you

- The original company you owed money to gave up trying to collect

The bad news? This can hurt your credit score. The good news? You have rights, and there are ways to deal with this.

Your Rights Under the Law

Before we jump into removing AssetCare from your credit report, let's talk about your rights. You have something called the Fair Debt Collection Practices Act on your side. This law says:

- Debt collectors must prove the debt is real

- They can't lie to you or trick you

- They must give you information about the debt

- You can ask them to prove you owe the money

Remember, just because they say you owe money doesn't mean you do. They need to prove it.

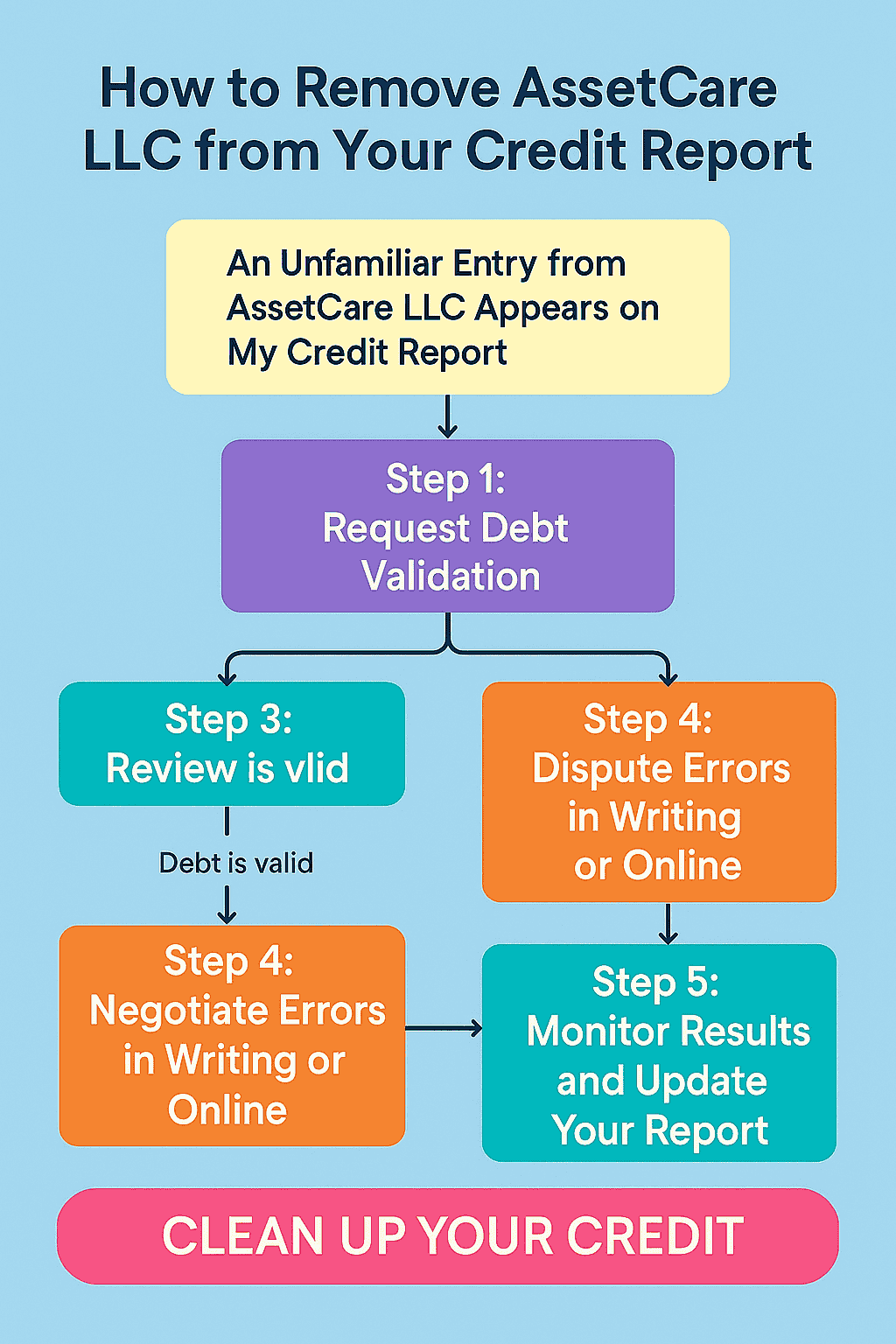

How To Remove AssetCare LLC from Your Credit Report

Step 1: Get Your Credit Reports

The first step is simple. Get copies of all three of your credit reports. You can get them free once a year from annualcreditreport.com. Look for any mentions of AssetCare LLC.

Write down:

- How much they say you owe

- When the debt started

- What the original debt was for

Step 2: Send a Debt Validation Letter

This is your secret weapon. Within 30 days of AssetCare first contacting you, send them a debt validation letter. This letter asks them to prove the debt is really yours.

Your letter should say:

- "I dispute this debt"

- "Please send me proof that I owe this money"

- "Show me the original contract or agreement"

Send this letter by certified mail so you have proof they got it.

Step 3: Check if the Debt is Too Old

Here's something many people don't know, debts get too old to collect. This is called the "statute of limitations." In most states, this is 3 to 6 years. If your debt is older than this, AssetCare might not be able to sue you for it.

Even old debts can still show up on your credit report for up to 7 years from when you first missed payments. But knowing if it's too old can help you decide what to do next.

Step 4: Dispute with Credit Bureaus

While you wait for AssetCare to respond, dispute the debt with all three credit bureaus, Experian, Equifax, and TransUnion. You can do this online or by mail.

Tell them:

- "I dispute this AssetCare LLC account"

- "This debt is not mine" or "This amount is wrong"

- "Please remove this from my credit report"

The credit bureaus have 30 days to check on your dispute.

Step 5: What Happens Next?

Now you wait. AssetCare has to respond to your validation letter with proof. If they can't prove the debt is yours, they should stop trying to collect it and remove it from your credit report.

If they do send proof, look at it carefully. Check:

- Is your name spelled right?

- Is the amount correct?

- Do the dates make sense?

- Is there a signature or contract?

Step 6: Follow Up

If AssetCare doesn't respond in 30 days, or if their proof doesn't look right, contact the credit bureaus again. Tell them AssetCare couldn't prove the debt. Ask them to remove it from your credit report.

Keep copies of everything. This paper trail is essential if you ever need to prove your case or dispute errors down the line.

We've outline the steps below:

Now, if you're trying to remove a collection account like AssetCare LLC from your credit report, you'll often hear the same standard advice like request debt validation, equifax disputes, or try to negotiate a settlement.

While these steps can help, many people don’t realize that credit repair professionals often use lesser-known but highly effective strategies. We’ll walk you through both the common advice and the more advanced methods as we go along.

Advanced Strategy To Remove AssetCare LLC

If you’ve already tried the basic steps, like mentioned above, but AssetCare LLC is still showing up on your credit report, don’t give up. There are more advanced, less commonly known strategies that credit repair professionals use to challenge these accounts more effectively.

These methods target legal compliance, reporting accuracy, and procedural weaknesses that can lead to the removal of the account entirely.

Portfolio Purchase Investigation

AssetCare buys debt in bulk portfolios. Use this to your advantage:

- Request the "Portfolio Purchase Agreement" that included your debt

- Ask for the "Chain of Title" documentation showing every transfer of your debt

- Demand the "Forward Flow Agreement" that governs how your debt was sold

- These documents are often incomplete or missing, creating grounds for dismissal

Sophisticated Validation Techniques

The "Prove Everything" Method: Your validation letter should demand:

- Original signed credit application or contract

- Complete payment history from the original creditor

- Proof of their legal standing to collect (assignment agreements)

- Calculation of the current balance including all fees and interest

- License to collect debts in your state

- Corporate authorization for the specific person contacting you

Sample Advanced Validation:

Under 15 USC §1692g, I dispute this alleged debt and request validation including:

1. Complete chain of title documentation from original creditor to your company

2. Original signed agreement establishing the debt

3. Itemized accounting of the balance including principal, interest, fees, and payments

4. Proof of your company's legal authority to collect this debt in [Your State]

5. Corporate resolution authorizing collection activities on this account

The "Furnisher Dispute" Method

Instead of disputing with credit bureaus, dispute directly with AssetCare as a "furnisher":

- Send disputes under FCRA Section 623(a)(8)

- Request "reasonable investigation" of disputed information

- Demand correction of any inaccurate data

- This puts burden of proof entirely on AssetCare

The "E-OSCAR Exploitation"

Credit bureaus use the E-OSCAR system for dispute processing:

- Submit very specific disputes that don't fit standard E-OSCAR codes

- Use technical language that requires human review

- Challenge multiple data points simultaneously to overwhelm automated systems

- Follow up with "inadequate investigation" complaints

Advanced Timing Strategies

The "Validation Trap":

- Send debt validation letter on day 29 of the 30-day period

- Simultaneously dispute with all three credit bureaus

- File complaint with CFPB about collection activities during validation period

- This creates multiple pressure points and potential violations

The "Reporting Window Challenge":

- Calculate the exact 7-year reporting period from date of first delinquency

- Challenge any reporting beyond this period

- Request removal based on expired reporting timeframe

The "Standing Challenge"

Question AssetCare's legal standing to collect:

- Demand proof they are the "real party in interest"

- Challenge their authority to report to credit bureaus

- Request the specific contractual language giving them reporting rights

- Many debt buyers lack proper standing documentation

State Law Exploitation

Research your state's specific debt collection laws:

- Some states require debt collection licenses

- Many have stricter validation requirements than federal law

- Some prohibit certain collection practices entirely

- Use state law violations in conjunction with federal claims

The "Regulatory Pressure Campaign"

File strategic complaints with multiple agencies:

- Consumer Financial Protection Bureau (CFPB)

- Your state Attorney General's office

- Better Business Bureau

- State debt collection licensing board

- Coordinate timing for maximum impact

Common Questions About AssetCare LLC

Let me answer some questions we get all the time:

"Can I just ignore AssetCare LLC?" Not really. Ignoring them won't make them go away, and the debt will still hurt your credit score. It's better to deal with it head-on.

"What if I really do owe the money?" If you owe the debt and AssetCare proves it, you can try to negotiate. Ask for a payment plan or see if they'll take less money to settle the debt.

"Will this hurt my credit score forever?" No. Most negative items fall off your credit report after 7 years. But dealing with it now can help your score sooner.

"Can AssetCare LLC sue me?" Maybe. If the debt is real and not too old, they might take you to court. This is another reason to handle it quickly.

When to Get Help

Sometimes you need backup. Consider getting help from a credit repair company or lawyer if:

- AssetCare won't work with you

- The debt is very large

- You're getting sued

- You don't understand your rights

Many lawyers offer free consultations for debt collection cases.

Preventing Future Problems

Here's how to avoid this happening again:

- Pay bills on time when possible

- Contact companies if you can't pay

- Keep records of all payments

- Check your credit report regularly

- Don't ignore debt collection letters

Final Thoughts

Dealing with AssetCare LLC on your credit report isn't fun, but you have options. Remember, you have rights. Don't let debt collectors push you around. Follow these steps, keep good records, and don't be afraid to stand up for yourself.

The key things to remember:

- Always ask for proof of the debt

- Dispute anything that looks wrong

- Know your rights under the law

- Keep copies of everything

- Don't ignore the problem

If you found this helpful, follow us on facebook and check out our other blogs about fixing your credit. Remember, knowledge is power when it comes to your credit report.

That's all for today's blog. Until next time, keep working on that credit score!

Disclaimer: This information is for educational purposes only and is not legal advice. Every situation is different. Consider talking to a lawyer or credit counselor about your specific case.

Related Read:

Who Is KLS Financial Services and Why Are They Contacting Me?

How Long Can Debt Collectors Legally Chase a Debt in California

5 Easy Steps To File an Effective Experian Dispute